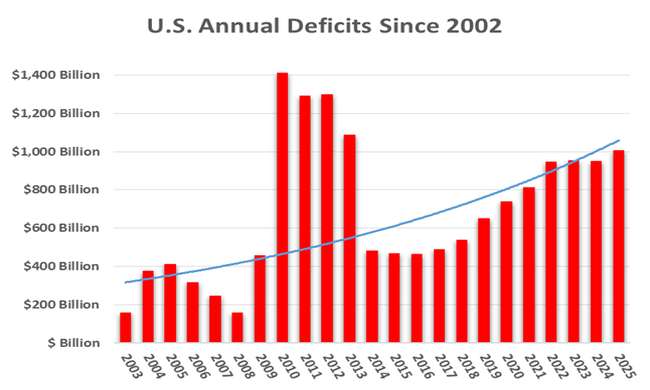

The idea of a balanced budget amendment to the U.S. Constitution (BBA) has been highly popular since the 1970s. Yet Congress has failed to propose a BBA, and the number of states applying for a proposing convention remains stuck below the necessary 34. Meanwhile, the federal debt continues to soar out of control.

Among the tactics employed by Article V skeptics is to highlight the difficulties in drafting an effective BBA. For once they have a point. Here are some of the defects afflicting present drafts, including some reproduced in Article V legislative applications:

*Relying on congressional supermajorities (two thirds, three fourths, 60%) whose practical effect will vary in unknown ways between the U.S. House and U.S. Senate.

*Unwittingly validating federal spending programs that, objectively considered, are currently unconstitutional.

*Introducing into the Constitution new words and phrases (e.g., “outlays,” “estimated revenue”), either undefined or poorly defined.

*Relying on budgetary formulae shown to be ineffective at the state level.

*Including terms (e.g., two-thirds vote to raise taxes) pleasing to potential donors, but rendering impossible the broad coalition necessary to ratify.

*Relying unduly on the courts for enforcement.

In addition, some of the drafts are simply too long to be accepted as amendments. The longest constitutional change ever adopted was the Fourteenth Amendment—containing 423 words—but some BBA drafts are far longer. In addition, some drafts contain unclear language. Consider this example appearing in a few state applications:

Total outlays of the government of the United States shall not exceed total receipts of the government of the United States at any point in time unless [a condition is met].

What does it mean to say that total outlays cannot exceed total receipts “at any point in time?” Does that mean that the inflow of dollars must always exceed the simultaneous outflow? Maybe. But if so, it disregards the realities of government finance: tax revenue arrives in chunks (as on April 15), while spending is more constant over the course of the year. Or does it mean that at any “point in time” all expenditures ever made, from 1789 to date, cannot exceed all funds received? But that would render existing debt unconstitutional. And what is a “point in time,” anyway? A day? hour? nanosecond? As Kurt Vonnegut might have quipped, “So it goes.”

Of course, it is one thing to criticize, but another to try to craft something better. II’s sister organization, the Heartland Institute, commissioned me to offer a suggested draft. It appears here, and includes detailed explanations. I know it is imperfect, and neither my draft nor anyone else’s should be included in state legislative applications. (The proposing convention has the constitutional prerogative of writing the amendment.) My goal is merely to “reset” public discussion to, perhaps, a higher level, and encourage others to offer proposals better than mine.