I’ve extolled the virtues of nuclear energy for its reliability, clean emissions, efficient land use, “just transition” potential, and energy security upside on several occasions.

I’ve even documented why many of the fears surrounding nuclear and aversion to its deployment are often irrational and misguided.

But one of the legitimate, good-faith critiques of nuclear is its track record of taking a long time to come online.

Indeed, the U.S. civilian nuclear industry is one of the worst offenders in this regard. Though it is often hampered by the onerous, risk-averse regulators at the Nuclear Regulatory Commission, the most recent reactor projects undertaken have suffered multiple construction delays. The only new nuclear reactors to be nearing completion this century are several years behind schedule.

Georgia’s Vogtle 3 and 4 reactors, approved in 2012, were originally scheduled to begin operating in 2016. The plant received federal approval to begin loading fuel in one of the reactors just last month.

And though a new class of nuclear entrepreneurs is looking to minimize this timeframe with smaller-scale advanced reactors, such projects are not yet far enough along the development curve to vindicate their promise of fast deployment.

What then, is a nuclear proponent to do?

After all, wind and solar are often quite fast to install these days, and advocates are claiming that makes them the more attractive option going forward.

“Nuclear is far slower to build than most other forms of power,” a New York Times columnist recently put it. “As battery technology improves and the price of electricity storage plummets, nuclear may be way too late — with much of its value eclipsed by cheaper, faster and more flexible renewable power technologies.”

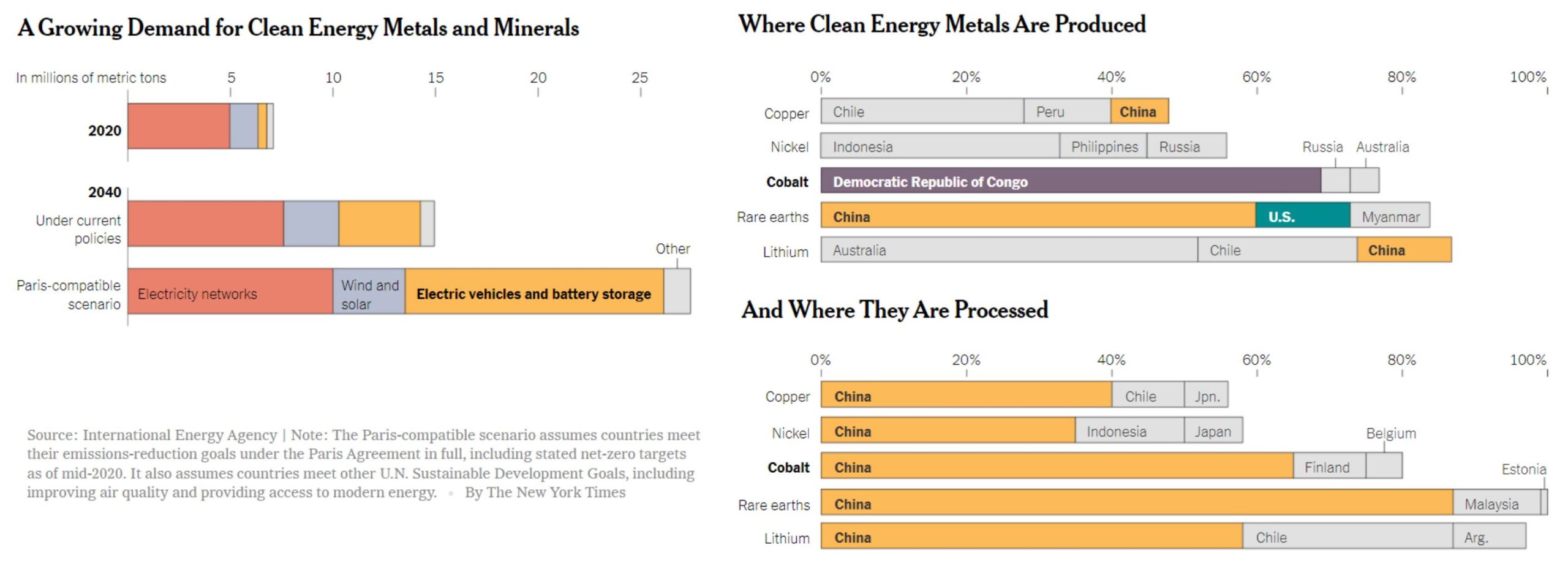

Except there’s just one problem. This sentiment, shared by many renewables advocates, seriously overestimates the readiness of critical minerals producers to provide the material inputs needed to facilitate an economy-wide build out of wind, solar, and batteries.

According to Utility Dive:

While a variety of metals like lithium, cobalt, manganese and nickel are fundamental elements in most EV batteries, copper has become the metal du jour. Its ability to conduct electricity well puts it in high demand not just for EV batteries, but electronics in general. Commodity analysts are raising red flags about an impending shortage.

S&P Global predicts “looming copper supply shortfalls” as global demand nearly doubles over the next decade, from 25 million metric tons now to 50 million metric tons in 2035. They attribute the projected surge to the rapid scale-up in demand for clean energy and decarbonization technologies containing copper, such as electric vehicles, batteries, charging infrastructure, solar panels, wind turbines and new transmission lines. Decarbonization goals “will be short-circuited and remain out of reach” unless significant new copper supplies quickly emerge, S&P Global suggests.

“At the same time demand is skyrocketing for these newer and growing markets, demand is holding steady or growing for copper in conventional applications such as pipes and wiring. S&P Global points to a decade of “massive underinvestment” in expanding existing copper mines or creating new ones as another factor fueling a supply crunch. New mines often take 15 to 20 years to come online, and permitting alone can take a decade.”

15 to 20 years for new critical mineral mining capacity.

In other words, the new mines desperately needed to supply the renewables industry with requisite mineral inputs take just as long, if not longer, than building out new nuclear plants. And that’s assuming that a renewed commitment to building new nuclear plants wouldn’t yield a high learning curve through subsequent builds.

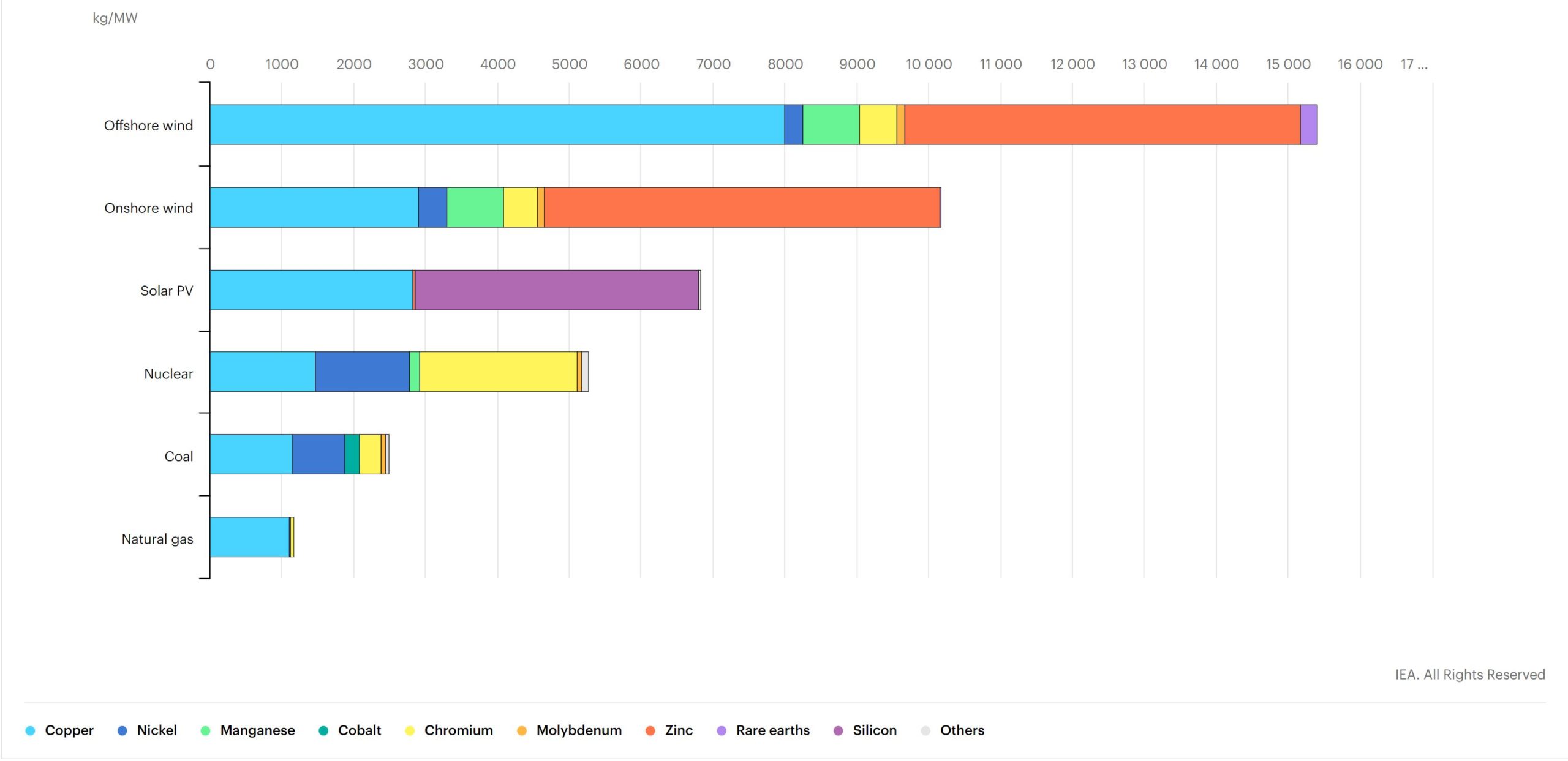

This is especially pertinent given the massive disparity in mineral requirements involved in the construction of renewables compared to nuclear facilities.

Plainly put, we’re making a political choice in pursuing one course of action over another. It certainly isn’t reflective of any real time-horizon advantages.

Renewables may be more nimble to deploy in the short-run, but the massive buildout imagined by the most ambitious of climate hawks is in for a very real supply constraint over the medium-to-long term. Demand for minerals is booming, particularly as governments increasingly commit to the most mineral-intensive resources available to meet our energy needs.

And with that booming demand interacting with a constrained supply, expect the decreasing prices that the renewables industry has seen over the last decade to face some seriously strong headwinds.

According to the International Energy Agency:

However, with major technological improvements achieved over the past decade, raw materials now account for the majority of total battery costs (50–70%), up from around 40–50% five years ago. Cathode (25–30%) and anode materials (8–12%) account for the largest shares.

Given the importance of material costs in total battery costs, higher mineral prices could have a significant effect on achieving industry cost targets.

There is good reason, according to the IEA, to expect mineral prices to continue rising due to supply-demand imbalances.

The picture for near-term supply is mixed. Some minerals such as lithium raw material are expected to be in surplus in the near term, while others such as battery-grade nickel or certain rare earth elements (REEs) (e.g. neodymium and dysprosium) might face tight supply in the years ahead.

However, after the medium term, projected demand surpasses the expected supply from existing mines and projects under construction for most minerals, meaning that significant additional investment will be needed to support demand growth.

But as noted above, that “additional investment” faces a 15-20 year waiting period in order to pay dividends. Such investment could easily be diverted to a less mineral intensive, baseload source of clean energy instead.

Such a plan would have major reliability advantages, as well as geostrategic ones. The current supply chain for critical minerals is dominated by our chief geopolitical foe.

Efforts to boost domestic mining capacity are worthwhile, and would be necessary even under a nuclear-heavy future scenario. But we should be under no illusion that it can happen overnight.

Reducing the 15-20 year lead time for new mining operations would require a major streamlining of permitting regulations, yet such regulatory reform could just as easily be applied to the already overburdened nuclear industry as well.

It all comes down to tradeoffs. Nuclear has indeed exhibited a propensity to take a long time to build in recent years, but it makes up for its slow construction time with long plant lifespans and high reliability once operational.

On the other hand, renewable projects are currently quick to deploy, but often have a quarter of the useable lifespan and an even smaller fraction of the reliability that nuclear facilities offer. And in the aggregate, a mass-scale buildout of renewable energy faces many of the same construction time delays exhibited by the nuclear power industry.

If there are good reasons to eschew nuclear as an answer to our low-carbon future, construction time isn’t one of them.