[vc_row][vc_column][vc_column_text]IP-8-2016 (November 2016)

Author: Joshua Sharf

DOWNLOAD REPORT IN PDF FORMAT

What is PERA?

Colorado’s Public Employee Retirement Association, PERA, is the public pension plan for Colorado’s state workers and public school teachers, as well as some local government employees. PERA has five major divisions, State Division, School Division, Denver Public Schools Division, Local Government Division, and Judicial Division. Far and away, the two largest divisions are the State and School Division.

PERA’s largest offering is its Defined Benefit plan, which promises lifetime benefits for retirees, based on age at retirement and years worked. It functions in lieu of Social Security for its active members. The plan is funded by a combination of government contributions and member contributions, which vary from division to division. PERA also offers a smaller Defined Contribution plan.

Executive Summary

In 2009, PERA’s own calculations showed that it would likely go broke sometime in the next 20-25 years. As a result, the legislature undertook significant reforms, lowering some benefits and increasing contributions.

While PERA’s funding level has stabilized since 2013, the reforms have been insufficient, and the underlying weaknesses have not been effectively addressed. The reforms have been insufficient, and PERA remains underfunded. Although many states have serious pension problems, Colorado’s is among the worst.

PERA reports assets with an actuarial value of $42.7 billion, balanced against reported accrued liabilities of $70.6 billion, for an overall funded ratio of 60.4 percent, and an unfunded liability of $27.9 billion. In reality, the funded ratio is significantly lower, and the unfunded liability for which the taxpayers are currently responsible is much higher, likely as much as $60 billion.

That staggering total amounts to over $30,000 in unplanned future payments for the average Colorado household.

Allocations to PERA already are taking resources from important government services, including schools. For the major suburban Denver school districts, PERA payments currently consume 12 percent of their annual operational expenses. If there are no reforms, that number will rise to over 20 percent.

PERA’s management incorrectly claims that its under-funding is primarily the resullt of state under-funding. In fact, employer under-funding is only one of several contributing factors. PERA’s problems are the result of poor investment allocation, overly generous benefits, and a willingness to sell future benefits to members at far below market value, especially in the late 1990s and early 2000s. PERA also systematically understates risk by understating the discount rate for its liabilities.

PERA’s funded ratio (currently 60.4 percent) has been worse in the past. However, two circumstances make a similar funded ratio more troubling now than before. First, PERA’s unfunded liability as a percentage of the state’s economic output has grown significantly. Second, the ratio of active members to beneficiaries has declined. The combined effect aggravates PERA’s burden on the state economy. Should a bailout be necessary, the responsibility will fall on the taxpayers, and not on PERA members.

Colorado’s problems are not unique, and the state has the opportunity to learn from the mistakes made and solutions implemented by other states. These solutions are readily implemented into both short- and long-term legislative agendas, beginning with transparency and accuracy, and ending with the transformation of PERA into a sustainable retirement program.

How Big Is Colorado’s Problem?

At the end of 2015, PERA reported an unfunded liability of $27.9 billion—only slightly smaller than the entire annual state budget, and roughly 8 percent of the state GDP.1 That is, PERA admits to having $27.9 billion more in promises, measured in today’s dollars, than it has money on hand to meet.

Underfunded pension plans have an amotization period, the time in which, given their expected rate of return on assets, they calculate they will be fully-funded. By law, the amortization period for the current year’s contributions is supposed to be 30 years. However, PERA reports 44 years for the State Division, and 50 years for the School Division.

There is good reason to believe that the situation is even worse than PERA admits.

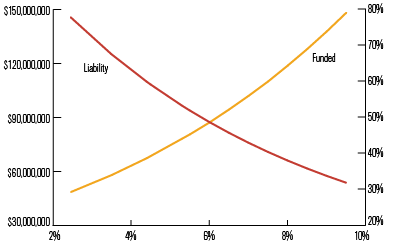

PERA reports a sensitivity analysis of its liability in its Comprehensive Annual Financial Report (CAFR), varying the expected rate of return from 6.0 percent to 9.0 percent, and discounting its future liabilities at the rate of return. The baseline rate of return was recently lowered from 8 percent to 7.5 percent, Moving to the lowest tested return of 6.0 percent, the unfunded liability balloons to $41.7 billion, or roughly 150 percent of the entire state budget.

However, using the rate of return as the discount rate understates the size of the liability.2 The discount rate is the interest rate that corresponds to the risk associated with PERA’s promises. Financial economics dictates that the size of a liability is independent of the return on the assets used the fund that liability.2 An appropriate rate of return for long-term contractual obligations is the state’s long-term cost of borrowing, about 5.3 percent for Colorado. In a recent report, Moody’s Investors Service used 4.4 percent as its discount rate.3 And during a recent debate concerning the possibility of issuing Pension Obligation Bonds, some investment bankers expressed confidence that the bonds could be issued at 3.5 percent.

Projecting the liability back to those discount rates results in significantly higher unfunded liabilities, as shown in figure 1:

A 5.3 percent discount rate produces an unfunded liability of $54.1 billion, and a funded ratio of 44 percent. More dramatically, a discount rate of 4.4 percent yields an unfunded liability of $67.4 billion, with a funded ratio of only 38.6 percent. The borrowing rate proposed by the investment bankers, 3.5 percent, yields an unfunded liability of $82.7 billion, and a funded ratio of 34 percent.

The Government Accounting Standards Board (GASB) recently took a step towards requiring an appropriate discount rate by requiring that any benefits not funded by current and future contributions for current and future retirees be discounted at government’s borrowing rate, producing a lower overall blended rate.4 A 2009 study by Boston College’s Center for Retirement Research found that applying GASB accounting rules shows that the School Division’s funding is only 52 percent, and the State Division’s is 48 percent.5

This accounting change was intended to more accurately reflect a plan’s underlying health. In reality, it may have the effect of encouraging pension plans to take on even more risk. The funded portion of a plan won’t change, but the unfunded portion will appear to grow, increasing the incentive to mask unfunded levels by investing in assets with higher returns, but greater volatility.6

In the event, the new GASB rule was determined to affect only the Judicial Division. In effect, given the 7.5 percent discount rate, and a 7.5 percent rate of return, all divisions except the Judicial Division will supposedly have sufficient assets on hand to pay benefits associated with current active and inactive members. We will discuss the validity of these assumptions later in this report.

Assuming a constant rate of return makes the modeling easier, but also fails to account for the real-world volatility of investment returns. Greater volatility increases the chance of one year of large investment losses, or several years of moderate losses. In such years, PERA will not have the option of cutting back on payouts, and will find itself trying to catch up from a lower asset base, having eaten its seed corn.

How Did We Get Here?

PERA’s problems result from several factors:

- The bursting of the dot-com bubble, and the 2008 market reaction to the financial crisis. The dot-com bubble was compounded by poor asset allocation

- An increase in benefits, including a decrease of the threshold for purchasing service credit

- Pension spiking, or gaming the system to inflate average salaries for the purpose of benefit calculations7

- The state’s failure to make its GASB Actuarially Required Contribution

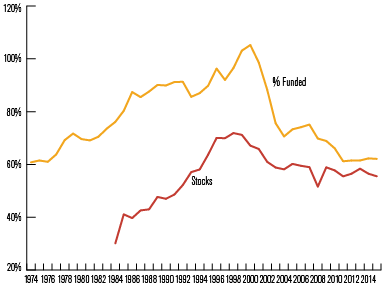

PERA began the mid-1970s with a funded ratio of roughly 60 percent, which improved to 75 percent by 1984. At that point, PERA’s portfolio was 30 percent equities. As shown in figure 2, it’s easy to see that PERA achieved full funding by 2000 as a result of letting the fund’s equity position grow to an dangerous 70 percent. When the dot-com bubble burst, so did PERA.

FIGURE 2

PERA Funded % and Stock % of Portfolio

Source: CAFR 1984 – 2015

By law, PERA’s equity holdings are not allowed to exceed 65 percent of its portfolio. However, that is calculated by cost-basis, not by current market or actuarial value of those investments.

Also during the late 1990s and 2000, the legislature expanded PERA benefits and refigured the retirement eligibility formula, making it more attractive to retire earlier. At the same time, the PERA Board made it easier to purchase service credit.8 The 1997 PERA law increased benefits by 25 percent, including raises for both future and existing retirees.

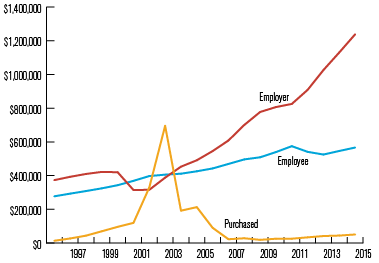

The effect on the unfunded liability was drastic. Figure 3 shows the sources of funds for the State and School Divisions. The effect of lowering the purchase price service credit for the state division to 15.5 percent, at the same time of making it easier to retire early, is evident. In 2003, the credit was the single largest source of funds, larger than either employer or employee contributions.

FIGURE 3

Contributions by Source – State and School Divisions

In 2003, the Board increased the price of purchased service credit to match the actuarial cost of benefits purchased after November 1, 2006. In 2004, the Board moved that deadline to November 1, 2005. But PERA is still on the hook for the many years of benefit credits that it sold at prices far below the cost of providing those benefits.

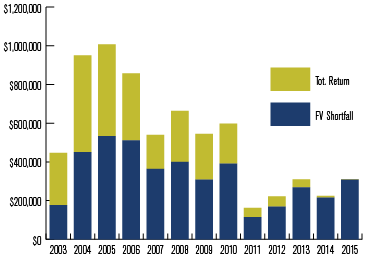

Another cause ofthe large unfunded liability is the state’s failure to make its Annual Required Contribution (ARC).

The ARC is set by a formula by the Government Accounting Standards Board (GASB), designed to keep the fund actuarially sound.9 PERA and its apologists often assert that the state’s failure is the sole cause for the parlous state of PERA finances. Actually, the state’s failure to contribute is responsible for no more than a quarter of PERA’s underfunding. Figure 4 shows the amount by which the state fell short of its ARC from 2003 to 2015. The bottom part of the column indicates the actual shortfall; the upper portion represents the total amount of interest that shortfall would have earned through 2014. Therefore, each column reveals the total amount that today’s PERA assets were underfunded as a result of each year’s shortfall.

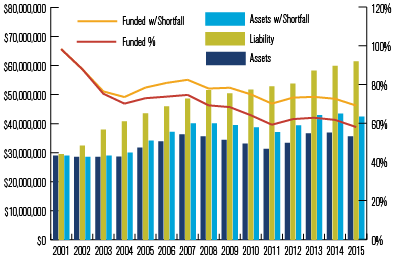

To date, this adds to a net shortfall in 2015 of $6.8 billion. PERA admits to an unfunded liability of $28.4 billion using the market value of its assets, and as we have seen, the number may be as high as $82 billion. As large a sum as $6.8 billion is, it’s only 25 percent of the smallest estimate.

Figure 5 shows the cumulative effect on the ARC shortfall, the amount that the legislature borrowed from the future by deferring payments, and the effect on the funded ratio.10

Different analyses arrive at different conclusions regarding how to apportion blame for PERA’s underfunding. In a detailed analysis of various causes, Josh McGee and Michelle Welch of the Laura and John Arnold Foundation place most of the blame on contribution deficits, attributing to them just under 50 percent of PERA’s current underfunding.11 They did not account for the portion of the underfunding problem caused by the purchased service credit “fire sale,” since the fire sale took place prior to the 2003-2014 period of the study.

The Sensitivity Analysis mandated by SB14-214 (see below), places half the burden on underperforming investment returns, and only about one third to contribution deficits.12 Unlike the Arnold Foundation Study, the Sensitivity Analysis covers the 16-year period from 1999 to 2014, which includes some of the fire sale.

Although the funded ratio has been even worse in the past, the problem of PERA’s long-term viability is worse than ever, for two reasons.

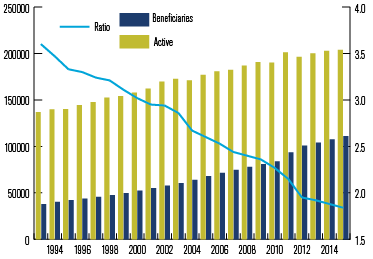

First, the ratio of current PERA members to beneficiaries has dropped sharply, from 3.5:1 to 1.9:1 over the last 20 years (see figure 6). Thus, when a bailout becomes necessary it will fall more heavily on the taxpayers than it would have in the past. There simply aren’t as many employees paying into the system per recipient as before.

FIGURE 4

PERA Contribution Shortfall

State & School Divisions ($000)

FIGURE 5

PERA Funded % w/Shortfall

State & School Divisions ($000)

FIGURE 6

PERA Participants

Source: US Census Public Pension Survey

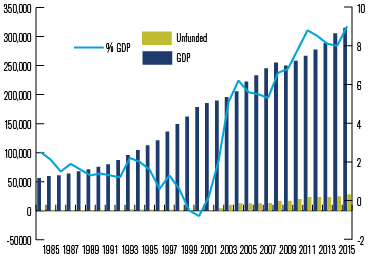

FIGURE 7

PERA and Colorado GDP

Unfunded Liability Based on Market Value of Assets ($000)

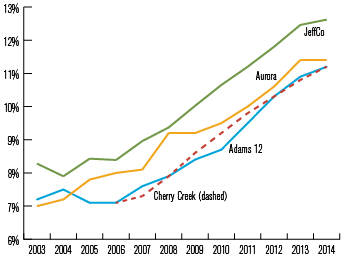

FIGURE 8

PERA as % of Operating Expenses

The second reason for concern is the size of the unfunded mandate in comparison to Colorado’s Gross Domestic Product (GDP). The ratio of unfunded mandate to GDP shows how burdensome a bailout would be to the state’s taxpayers. The higher the ratio, the harder it will be to bail out the fund when that becomes necessary. The amount of resources available to taxpayers to fund such a bailout is directly related to the size of the state’s economy.

Through the late 1990s, PERA’s admitted unfunded liability amounted to about 2 percent of the state’s GDP. Now, the unfunded liability is nearly 9 percent of state GD. Thus, PERA is all the more vulnerable to any future cyclical downturn in tax revenue.

A Matter of Fairness

PERA’s unfunded liability and the growing taxpayer contributions necessary to maintain PERA’s solvency pose a long-term threat to the state’s finances and its ability to carry out its responsibilities.

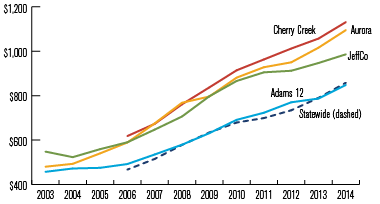

Colorado faces three options. 1) retirees and those near retirement get lower benefits than they were promised, 2) cut public services to pay for retirement benefits, or 3) raise taxes—thus making taxpayer pay the pensions of people who were allowed to retire much earlier than most taxpayers can. Each option is fundamentally unfair. In effect, option 2 is already being implemented in several large school districts, with money being diverted from classrooms,13 as shown in figure 8.

The increase began with the 2006 law requiring employers to pay an Amortization Equalization Disbursement (AED) and have continued to grow with SB10-001’s Supplemental AED (SAED) requirements. The employer contributions have been growing considerably faster than the rate of inflation for some time (see figure 9).

FIGURE 9

PERA per Student

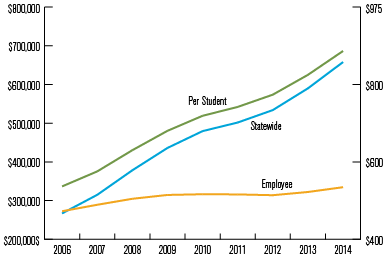

These increases represent dollars being diverted from the classroom to teachers’ retirements, dollars coming largely, although not entirely, from the taxpayers. In figure 10, the Statewide Employer and Employee contributions are shown on the left axis, while the per-student cost is shown on the right.

The increase in the per-student contribution closely tracks the increase in employer contributions, and is now over $850 per student statewide. The employee contribution has remained basically flat since 2008. This is despite the stated intent of both lawmakers and PERA that the SAED burden be shared between employers and teachers.

This level of growth in taxpayer PERA contributions is unsustainable. While the State Division hasn’t yet seen a similar level of growth, eventually the state budget will see similar stress. Legislators will be forced to choose among taxpayers, beneficiaries, and basic services.

FIGURE 10

PERA School Div. Contributions

(left axis $000)

SB14-214 Required Reports

Overview

In 2014, the legislature voted to commission three separate studies, to be conducting by an independent auditing firm with PERA’s cooperation.

The first report was an analysis of PERA’s hybrid plan structure.14 It included a comparison of PERA’s benefits with those available nationally, and a comparison of the current Defined Benefit plan with alternative Cash Balance and Defined Contribution plans. It also examined the transition costs associated with moving to one of the other plan structures.

The second was an exploration and proposal of simplified status metrics designed to provide policy-makers an early-warning system in the event that PERA was beginning to stray from the recovery path laid out in SB10-001.

The third was a comprehensive audit of PERA’s books. This was not an evaluation of PERA’s long-term health or fiscal soundness, rather it was an evaluation of PERA’s accounting. PERA received a clean bill of accounting health.

Hybrid Plan Study

The two main elements of the Hybrid Plan Study are a comparison with benefits provided by other states, and a comparison with other proposed plan structures.

Comparison with other state benefits

The Study argued that PERA’s benefits were on a par with those offered in other states. Because PERA replaces Social Security for its members, the study considered PERA’s peer group to be other statewide and teacher defined benefit plans that also do not participate in Social Security. It found five peer statewide plans, and ten peer teachers plans.

Using a baseline of an employee retiring at age 65 with 30 years of service, PERA’s replacement ratio – the percentage of the final year’s salary that the retiree would draw in pension – was calculated to be 72.2 percent. Three of the other five statewide plans matched that, as did four of the other ten teachers plans. None exceeded it.

The Study found the effects of other elements of the plans – COLAs, eligibility requirements, for example – to be small by comparison, and generally to balance each other out. Therefore, the study concluded that PERA’s benefits were comparable to those in other states.

On the other hand, in 2014, Andrew Biggs of the American Enterprise Institute compared both the replacement ratios and the absolute benefit amounts earned by full-career retirees for all plans.15 He found that while Colorado’s replacement rates were average, the annual and total benefits earned were among the highest in the nation.

A 2014 study by the Urban Institute used a grade system to evaluate each state’s public pension systems on benefits and funded level.16 It agreed with AEI’s conclusions that PERA serves career employees exceptionally well, giving the State, Local, and School Funds A grades for “Retirement Income for Long-Term Employees.”

Where the Urban Institute failed PERA was on Rewarding Younger Workers and Encouraging Work at Older Ages. Both the State and School Divisions received D grades for Retirement Income for Short-Term Employees. The contributions from short-term and younger employees are being used to fund the high benefits enjoyed by employees who retire with many years of service.

The National Council on Teacher Quality (NCTQ) evaluated PERA’s School Division in comparison with other states, and on various specific criteria. Taking into account portability, stability, funded level, and fairness in vesting, they gave PERA a C-, along with most other states.17

The report notes that benefit structures such as PERA’s, that have long vesting periods, are unfair to teachers, and make it harder to recruit and retain qualified teachers.

Comparison with other Plan Structures

The Hybrid Plan Study compared PERA’s current hybrid Defined Benefit plan with two other widely-used plan models: the Defined Contribution and the Cash Balance plans. In addition, the Study compared a “Side-by-Side” plan, where “the state contribution funds the defined benefit portion of the plan and the member contributions fund the defined contribution portion of the plan.”18 The study only encompassed the State Division.

A Defined Contribution (DC) plan operates like a 401(k) plan. Individuals and their employers contribute a set amount of pre-tax money based on salary and tenure. The money is then invested, and upon retirement, the member can draw from that account, and pay income tax on the withdrawals. The employee is not guaranteed a rate of return, a balance, or any annuity, only the assets invested in his or her name. By definition, therefore, a DC plan is always 100% funded.

A Cash Balance (CB) plan is structured somewhere in-between a DB and a DC plan. It guarantees the employee not an annuity, but a specific cash balance upon retirement, based on age, years of service, and salary. While the employer assumes the investment risk up to the point of retirement, the employee assumes all post-retirement risk.

In order to compare the three plan structures, the analysts ran two experiments. First, they ran essentially the inverse experiment, calculating the amount employers and employees would need to contribute in order to provide the same benefits. This is called the “Targeted Benefit Approach.” Then, they kept the amount invested constant, and calculated the benefits retirees could expect to receive. This is called the “Targeted Contribution Approach.”

In all three cases, under both approaches, the current Hybrid Plan was the clear winner. Under the Targeted Benefit Approach, the Side-by-Side DB/DC plan would require 60 percent greater contributions to achieve the same benefits, the Cash Balance plan would need 79 percent more, and the Self-Directed DC plan a whopping 142 percent greater contribution to achieve similar replacement ratios, nearly two-and-a-half times the current contribution.19

The Targeted Contribution Approach looks even more dire for retirees. For the same amount invested, the Side-by-Side DB/DC approach provides only $0.75 for every dollar in current benefits, the DC plan just under 40 percent, and the Cash Balance Plan would leave its members struggling to get by on only a little over one-third the benefits.20

But the findings that the current version of PERA is better than any alternative were based on an unrealistic assumption: that the other plans would achieve only a 5.5 percent annual return, two full percentage points below PERA’s supposed 7.5 percent return. The justification for claiming that PERA would produce a 2% better return was that PERA would get better investment advice and that its management costs would be lower.21

These assumptions stacked the deck in favor of the current plan structure.

In December 2015, the Center for Retirement Research at Boston College published its own study, indicating that the return differential between Defined Benefit and Defined Contribution plans was closer to 0.7 percent, rather than 2.0 percent, notiong that “Since this differential remains even after controlling for size and asset allocation, the likely explanation is higher fees in defined contribution accounts.”22

However, the fee impact between the plan types can be eliminated completely by allowing PERA to remain the investment manager of choice for PERA members. PERA would continue to exercise its investment expertise on behalf of its members, continue to benefit from lower transaction costs, and better access to markets. It would simply manage the money on behalf of a different plan structure.

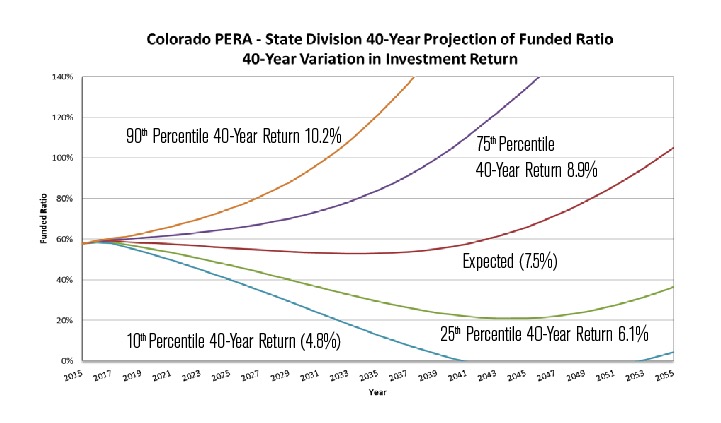

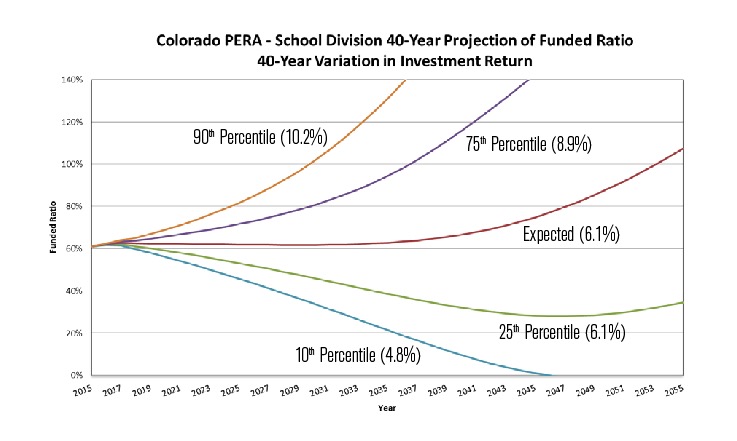

Sensitivity Analysis

In October 2015, the State Auditor’s Office delivered the last of the SB14-214-mandated reports, the Sensitivity Analysis of PERA Actuarial Assumptions.23

The report performed a sensitivity analysis on PERA’s future based on four factors:

- Investment Return,

- Salary Growth,

- Population Growth, and

- Other Actuarial Experience such as longevity.

Of these four, the report found PERA’s future solvency to be most dependent on Investment Return, which also had the highest degree of uncertainty associated with it.

In addition, the study proposed a “Signal Light” system for reporting PERA’s status, as a means of providing a simplified but comprehensive overview of PERA’s current state and likely future.

There is much to commend in the report’s approach and thoroughness. While we have some differences with the way the long-term curves are calculated, our major concern centers around the willingness of policy-makers to heed the warning signs.

Measures of Fundedness

The study considered a number of measures of fundedness before settling on two: the Funded Level and the Amortization Period.

The Funded Level is the percentage of a plan’s promises that it has the assets to cover. The Amortization Period is the time until a plan is expected to be fully-funded. While the Funded Level gives some measure of the current position of the plan, the Amortization Date can give a measure of how well PERA is adhering to the plan laid out in SB1. At the moment, the Amortization Period improves at about one year per percentage point of return in excess of the 7.5 percent expected return; the Amortization Period recedes one year into the more distant future for each percentage point that PERA’s investment return falls short of a 7.5 percent annual return.24

Long-Term Projections and Variations

In analyzing PERA’s sensitivity to investment returns, the Study used a number of variations on the baseline case of 7.5 percent annual returns. It takes the standard deviation of returns over the last 15 years, 1999-2014, and applies that spread to the mean expected return of 7.5 percent. Assuming a normal distribution, it can easily determine the distribution of 40-year returns, and the baseline, 25th-percentile, and 10th-percentile cases for the next four decades.

One example, showing the projected funded levels for each of those return profiles over the next forty years, is shown below:

As these graph shows, the State Division has a 25% chance of falling to a 20% funded level thirty years from now; the School Division has that same chance of falling to only 25% funding in that same time period. A 40 percent funding level is considered dangerously low, and it appears that PERA’s State Division stands a 1-in-3 chance of falling to that level or worse in the next several decades.

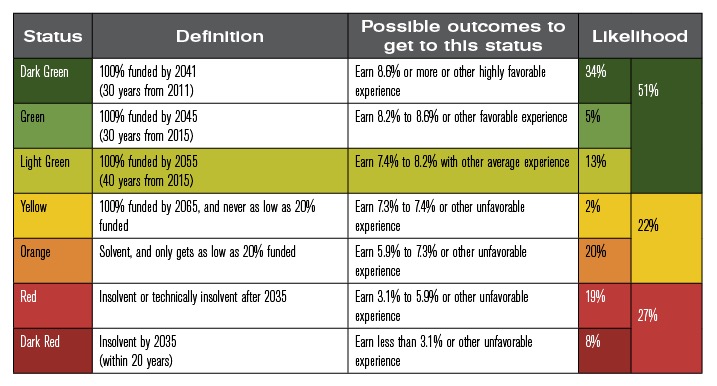

Signal Light Measures

The Study developed a Signal Light mechanism to display PERA’s status in a relatively simple way for policy-makers, with colors ranging from dark green (best), to yellow, orange, and dark red (worst). The color of the signal light depends most on the relative likelihoods of various Amortization Dates.

The study back-tested the system as far back as 2008, to show that it would have signaled trouble prior to the 2008 market crash and subsequent adoption of the SB10-001 reforms.

The current chart for the State Division is shown below:

While the overall color is light green, a 51 percent chance of being funded 40 years from now still leaves the plan with nearly a coin-flip’s chance of not being funded in that time period, and a 47 percent chance of never being fully funded.

Objections

The Sensitivity Study contributes significantly to understanding of PERA’s situation.25 By extending the analysis over time, and over a wide, plausible range of return profiles, the Study helps policy-makers and analysts visualize the long-term effects of the return profile. It is a commendable first effort, and should be incorporated annually into PERA’s reporting.

That said, the Study does have shortcomings.

Discount Rate

The study uses the expected rate of return as the discount rate for the plan liabilities. We have previously discussed why this rate understates PERA’s liability, the extent of the underfunding, and the amortization periods. Using the 7.5 percent discount masks the severity of PERA’s problems.

Incorrect Return Profiles

The study makes a number of questionable assumptions about PERA’s likely investment return profile. First, it assumes that investment returns are normally distributed, as in a bell curve. Considerable research indicates that investment returns are not normally distributed.26

In addition, the calculations are based on PERA’s historical returns as a whole, rather than on the returns on the individual asset classes comprising its portfolio. As we have seen, the mix of asset classes has varied significantly.

Finally, in order to make the calculations easier, the study uses deterministic rather than stochastic calculations. A stochastic return model would vary the returns from year to year based on historical returns on the portfolio components. Instead, the study authors used a series of constant returns over the projected period.

While this has the benefit of allowing the analysts to impute a single return to the 25th- and 10th-percentile, it has the disadvantage of failing to account for individual years that may be very good or very bad. Recent history has shown that even several very good years do not suffice to dig a plan out of a couple of bad years, or one very bad year such as 2008. Even after a bad year, a plan still has to make payments to its retirees, and could find itself spending principal, depriving it of the investment gains on that money.

Using a stochastic model would still allow for statistical results at every year along the curve, without the simplifying and potentially misleading assumption of constant returns, and it would also make it easier to rectify the other statistical shortcomings mentioned above.

Different Effects in Future

PERA’s contribution and payout profiles are projected to change considerably over coming years. That is why a funding ratio of 60 percent in 2015 precedes decades of underfunding, while the same funding ratio thirty years from now marks the projected beginning of a steep rise in funding.

It stands to reason, then, that significant departures from the expected rate of return would have different effects on the plan’s future, if they occur at different points along the line. By using a constant rate of return for all plan years after 2030, in all scenarios the study cannot show these effects. There may be particular years that, because of changing demographics or financial profiles, hold particular risks for PERA’s funding.

Signal Light masks risks

Finally, as mentioned above, the Signal Light Report has the potential to mask significant risks. Currently, the State Division’s color is reported as Light Green, but that division has a nearly 50 percent chance of never being fully funded.

National Context

PERA’s problems are part of a national pattern, with public pensions all across the country putting state and municipal governments under pressure.27 The collective national unfunded liability in 2013 was reported by the pension funds themselves to be $1.15 trillion, and outside experts estimate unfunded liability as high as $3 trillion.28

One 2009 study found that “A larger number of public pension plans have zero probability of paying accrued benefits than have a probability in excess of 50 percent.”29 In other words, the number of plans that have no chance of living up to their promises is greater than the number of plans that have a better than even chance of making all the payouts.

Several funds are in particularly bad shape. Illinois Teachers’ State Retirement System executive director Richard Ingram has said that his fund, which reports being 46 percent funded, may go bankrupt by 2030.30 The demands of paying for the California Public Employees’ Retirement System, CalPERS (possibly 40 percent funded31), and the California State Teachers’ Retirement System, CalSTRS (less than 70 percent funded32) have forced California to increase taxpayer contributions by 50 percent over six years.

In Pennsylvania, a recent auditor’s report found that nearly half of the state’s municipal pensions are underfunded, with one in ten under moderate or severe distress, meaning that they are at least 30 percent underfunded.33 As of 2012, one in every six dollars of spending from Philadelphia’s general fund went to pensions, squeezing out other services.34

Pension plan demands have driven a number of cities and counties into bankruptcy or near-bankruptcy. These include the cities of Stockton,35 San Jose, Vallejo, and San Bernadino in California; Jefferson County in Alabama; and Harrisburg and Scranton, Pennsylvania.36

Several states and cities have taken steps to scale back pension benefits and shore up funding. Utah, Michigan, and Alaska all have begun to move new hires into 401(k)-type defined contribution plans. Other municipalities have reduced or frozen COLAs (Cost of Living Adjustments), or changed the formulas by which they are calculated.37 Retirees in Providence, Rhode Island, recently agreed to a COLA freeze and changes in health benefits.38 And two large California cities voted to change their respective systems: San Jose will cut benefits and increase employee contributions, while San Diego will freeze benefits and put new workers into a defined contribution plan.39

In the face of mounting worries about long-term obligations and their effects on their communities, a number of states have taken action to reform their pension systems in recent years. The California Public Employees Pension Reform Act (PEPRA) provided many measures aimed at reducing benefits and raising contributions of new employees.40 These included capping pensionable income, basic benefits on an average of the last three years, and other changes to the pension formulas. However, the reform has been ineffective, perhaps due to a restrictive definition of “new employees.”41

Other states have also implemented reforms. Nevada has reduced the annual pension increases for retirees, and switched from a three to a five year period for calculating highest annual earnings.42 However, legislation to make a major switch to a DC plan was pushed off.43 Effective November 2015, all new Oklahoma hires are given a defined contribution plan.44 The only exceptions will be hazardous-duty employees and teachers.45 Texas has approved contribution increases for education workers.46

The Pennsylvania has struggled to pass legislation enrolling new employees in a hybrid plan consisting of a traditional pensions fund and a 401(k)-style plan.47 This comes after Gov. Tim Wolf vetoed a bill which would have switched to a completely DC plan.48 In 2012, Louisiana replaced its defined benefit plan with a cash balance plan for all new employees.49 Also a new bill (HB 65, HB 66) has been introduced to switch to a hybrid plan for all new employees.

Kansas has taken multiple actions. A 2012 reform lowered the guaranteed investment return for employee accounts, and shifted gaming revenue to pay down its public pension debt.50 The 2012 legislation took steps to reduce double dipping.51 In 2015, more double-dipping reforms were enacted.52

Recent Attempts at Reform

In the past several years, Colorado has passed several PERA reform bills. One was aimed at reducing the state’s unfunded liability, while the others provided temporary fixes designed to relieve immediate budgetary pressure.

SB10–001

In 2010, Colorado Senate Bill 1 significantly adjusted PERA’s benefit calculations:

- COLAs were capped at the lesser of 2 percent or inflation.

- The practice of double-dipping by PERA-covered employers was ended.

- Retirement age was raised to 58 from 55 for most new hires after January 1, 2011.

- The salary used for calculating benefits was spread out over the last 5 years of service, and limited to raises of 8 percent per year.

These changes, while reining things in at the edges, left intact the overall defined benefit structure. For that reason, they survived a prolonged legal challenge, with the Colorado Supreme Court ruling on October 20, 2014 in Justus v. State53 that the adjustments to PERA’s COLAs were permissible under both the state and federal Constitutions.

SB10–146, SB11–076

These two laws shifted 2.5 percent of the annual PERA contribution from the state to the employees, at a savings of roughly $20 million per year. Each was a one-time budget fix, and neither was repeated thereafter.

Policy Proposals

The ultimate answer to Colorado’s fiscal problem is to follow Utah, Alaska, Michigan, Rhode Island, and San Diego in transitioning to a defined contribution (DC) plan, following the private-sector trend.54 Such a transition, done well before the crisis stages, carries a net benefit for all parties concerned—the employees, the state, and the taxpayers—by limiting the potential long-term liability and converting to a plan that is by definition actuarially sound.

In a defined benefit (DB) plan, a member receives a promise that the employer will pay a benefit in the future. As we have seen, there may or may not be sufficient funds to cover the obligations. A defined contribution (DC) plan, by contrast, is by definition always fully funded. The beneficiary owns an asset, and can access the value of that asset. There are no unfunded promises, because none are made.

The main financial reason usually given for refusing to convert from defined benefit to defined contribution is the transition cost, defined as a change in the way that future obligations are scheduled to be paid.

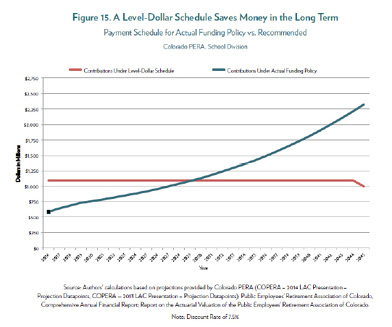

There are two ways to amortize a long-term pension liability: Level Dollar, which assumes equal payments over the 30-year window, and Level Percent of Pay, which assumes that the payments stay level as a percentage of the participants’ salaries, but that the salaries rise. Level Dollar amortization costs less over the life of the debt retirement, but costs more now, at a time when state budgets are already tight. Level Percent of Pay costs more, but pushes much of that cost into the out years.55

GASB rules state that when a defined benefit plan closes, it must change from Level Percent of Pay Amortization to Level Dollar amortization, for purposes of calculating its ARC. The effect is to shift amortization payments from later years to earlier ones.56

However, economist Josh McGee points out that this change only affects financial reporting, and doesn’t actually require any additional payments be made sooner. The method of funding the liability can be independent of its financial reporting, meaning that no actual payments need to be made sooner.

FIGURE 11

Most important, a transition, accompanied by a “hard freeze” in benefits—leaving vested benefits untouched, but accruing all new benefits in a defined contribution plan—caps the unfunded liability. It does not eliminate the unfunded liability. It does, however, prevent the liability from growing.

Remember that a defined contribution plan is by definition fully funded, and under a “hard freeze,” no more liabilities can accrue under the DB plan.57 The state will be left with the same liability, and the same obligation to fund it. The plan can be no worse off than it is now, and by capping the risk associated with its unfunded liability, it can end up in considerably better shape than it otherwise would have been.

Intermediate Proposals

In order to build support for such a significant shift, the State may wish to take intermediate steps both to put the plan on sounder footing and buy time, while increasing transparency and accuracy in reporting.

In the shorter term, PERA would also benefit from lowering its expected rate of return, as it has twice in the recent past. The current expected rate of return is 7.5 percent. Since PERA uses the expected rate of return as the discount rate, lowering it would have the effect of increasing the UAAL, and more accurately reflecting PERA’s true funded state.

Further, a more realistic expected rate of return would PERA’s incentives to add risk, and therefore volatility, to its portfolio.58 The California State Teachers Pension (CalSTRS) has recently decided to phase in a reduction in its expected rate of return from 7.5 percent to 6.5 percent, specifically in order to reduce the risk in its portfolio.59 Despite the recent rate reductions, PERA’s current portfolio still carries a significant risk premium.60

A number of other bills have been introduced into the legislature in recent sessions. Many of these ideas were drawn from the Independence Institute’s Citizens Budget61, a comprehensive look at state fiscal policy. While none of the following proposals were enacted into law, they are all good ideas that would make PERA stronger:

- SB12–016: Local Government Option to Change PERA Contributions

Would have allowed local governments to shift a portion of the employer contribution to the employees, an option available to state government. - HB12-1250: Health Care Benefit

Would have recalculated the Health Care Division contributions as a function of health care costs, based on current subsidies paid out, rather than employees’ salaries. - SB12-082: PERA Retirement Age Equal to Social Security

Would have set the PERA retirement age equal to the retirement age for Social Security, as a matter of fairness to the taxpayers supporting the system. - SB12-119: PERA Fiscal Sustainability (30-Year Amortization)

Would have required PERA to adjust its benefits and contributions whenever the amortization period for a given division exceeds 30 years. - SB12-136: Include Retirement Benefits in Biennial State Compensation Report

Would have included PERA costs and recommendations in the state personnel director’s compensation report, to be prepared biennially instead of annually, as is now the case. - SB13-055: Actuarial Soundness

Would have required PERA to use the state’s long-term cost of borrowing to discount its liabilities, and would have required benefit and contribution changes to bring the individual funds’ amortization periods under 30 years. - HB12-1142: Allow all PERA Employees Access to Defined Contribution Plan

Would have opened up access to PERA’s defined contribution plan to all PERA employees, rather than only certain state employees. - SB12-1179: PERA Board Composition

Would have reduced the confict of interest (known as the agency problem) on PERA’s board by removing elected board positions, and replaced them with board positions filled by non-PERA employees and beneficiaries. - SB14-068: Retirement Age for PERA Members

Would have gradually raised the retirement age for PERA members until it reached age 65. - SB15-080 Participation In PERA’s Defined Contribution Plan

Would have expanded the option to participate in PERA’s defined contribution plan to all participants in the State and School Divisions

Pension Obligation Bonds

In 2015, the Colorado legislature took up the question of issuing Pension Obligation Bonds (POBs) to shore up PERA. HB15-1388 would have authorized the State Treasurer to issue up to about $10 billion in bonds, on the credit of the State of Colorado, to increase PERA’s assets. The interest on the bonds would have been paid primarily by the AED and SAED already in the income stream, so the likelihood of actually defaulting on the bonds was relatively low.

The bonds would have done little to help PERA’s finances. Supporters of the bonds argued that it amounted to refinancing a portion of PERA’s debt with bonds whose interest was expected to be around 3.5 percent. That calculation depended on using the 7.5 percent discount rate from the expected rate of return on investment. However, if the correct discount rate of about 3.5 percent were used, the net effect would have been to add up to $10 billion in both assets and liabilities. While this would have increasing the funded ratio side of PERA’s books, it would not have reduced the unfunded liability at all.

Political Challenges & Opportunities

Colorado faces a distinctive political landscape in trying to enact change.

In 2007, Gov. Bill Ritter signed an executive order permitting state employees to unionize, a move that current Gov. John Hickenlooper has thus far retained. While Colorado WINS has failed to recruit more than a handful of state employees to its ranks, it is possible that a serious threat to employee pensions—real or imagined—could spark a reaction.

PERA’s former Executive Director Meredith Williams has strongly defended defined benefit plans, dismissing criticism of them as “allegations.” Among the “allegations” are that defined benefit plans are overly optimistic in their returns assumptions, that they are headed toward insolvency, that they have received and will need taxpayer bailouts, and that they should include defined contribution options.62 Far from being mere allegations, they are matters on which almost all serious financial economists agree.

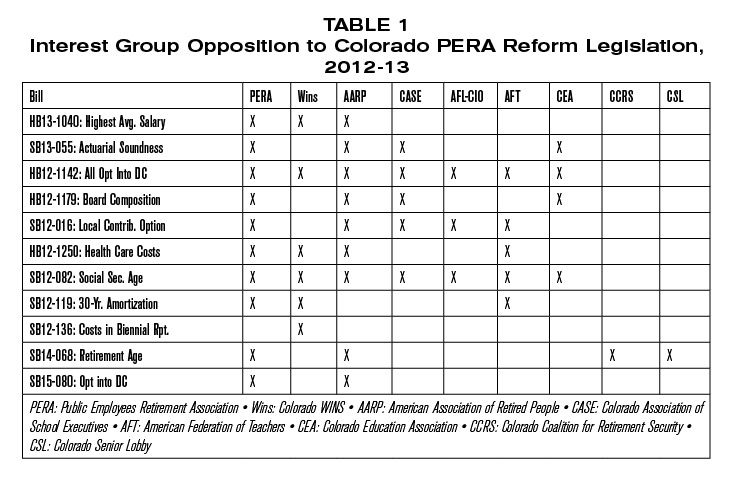

PERA opposed all but one of the 2013 reform bills. Other public employee lobbies often joined the opposition (see table 1).63

Nevertheless, experience in other states suggests that alliances across ideological lines may be possible. In both New York and New Jersey, private sector unions, recognizing the threat that increasing contributions to public sector pensions pose to their own members’ livelihoods in the form of public works, have joined with governors to implement changes to the system.64

There is also the possibility that pension funds’ investments in riskier assets in order to meet investment targets will lead to resentment among those who distrust Wall Street investment firms.65

PERA does not face immediate catastrophe. It does need to take immediate steps to prevent eventual default. Were default to occur, the persons most hurt would be those least able to make adjustments in their personal finances: those already retired, and those nearing retirement. The situation facing current retirees in Detroit need not be Colorado’s future. It can be avoided by reasonable, fair, common-sense changes now.

Glossary

AED – Amortization Equalization Disbursement

AEI – American Enterprise Institute

ARC – Actuarially Required Contribution

CAFR – Comprehensive Annual Financial Report

COLA – Cost of Living Adjustment

CalPERS – California Public Employees’ Retirement System

CalSTRS – California State Teachers’ Retirement System

DB – Defined Benefit

DC – Defined Contribution

GASB – Government Accounting Standard Board

GDP – Gross Domestic Product

NCTQ – National Council on Teacher Quality

PEPRA – California Public Employees Pension Reform Act

PERA – Public Employees Retirement Association

POB – Pension Obligation Bonds

SAED – Supplementary Amortization Equalization Disbursement

UAAL – Unfunded Accrued Actuarial Liability

Endnotes

1 Bureau of Economic Analysis, “Widespread economic growth across states in 2011,” June 5, 201. https://www.bea.gov/newsreleases/regional/gdp_state/2012/pdf/gsp0612.pdf

2 Lawrence N. Bader and Jeremy Gold, “Reinventing Pension Actuarial Science,” April 17, 2003, Society of Actuaries. https://www.soa.org/library/newsletters/pension-forum/2003/january/pfn-2003-vol14-iss2-bader-gold-a.aspx

3 Moody’s Investor Service, “Adjusted Pension Liability Medians for U.S. States,” June 27, 2013.

4 Mary Williams Walsh, “New Rules on Pension Funds Seek Better Disclosure,” New York Times, June 24, 2012.

5 Alicia H. Munnell, et. al., “How Would GASB Proposals Affect State and Local Pension Reporting?” CRR Working Paper 2012-18 (June 2012). https://crr.bc.edu/wp-content/uploads/2012/06/wp_2012-17.pdf

6 Andrew Biggs, “Public Sector Pensions, How Well Funded Are They, Really?” State Budget Solutions (July 2012), https://www.statebudgetsolutions.org/publications/detail/public-sector-pensions-how-well-funded-are-they-really

7 Michael V. Mannino and Elizabeth S. Cooperman, “Benefit Enhancement in Public Employee Defined Benefit Pension Plans: Evidence From Three Sources,” University of Colorado Denver, Business School, January 24, 2013. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2206656

8 Public Employee Retirement Association Comprehensive Annual Financial Report, 2000.

9 “Pension Fund Actuarial Required Contributions (ARC),” The Civic Federation, February 14, 2007, https://www.civicfed.org/sites/default/files/civicfed_241.pdf

10 PERA Comprehensive Annual Financial Reports, 2001-2014. https://www.copera.org/investments/pera-financial-reports

11 John McGee, Michelle Welch, “Risky Retirement: Colorado’s Uncertain Future and Opportunities for Reform,” Laura and John Arnold Foundation, June 2015. https://www.arnoldfoundation.org/wp-content/uploads/2015/07/Risky-Retirement_Colorados-Uncertain-Future-and-Opportunities-for-Reform.pdf

12 “Sensitivity Analysis of Colorado Public Employees’ Retirement Association Hybrid Defined Benefit Plan Actuarial Assumptions,” October 2015, Pension Trustee Advisors, prepared for the Colorado State Auditor’s Office, P. 23

13 Jefferson County Public Schools, Comprehensive Annual Financial Reports, 2005-2011, Budget 2012. https://www.jeffcopublicschools.org/finance; Aurora Public Schools, Comprehensive Annual Financial Reports, 2005-2011, Budget 2012, https://aurorak12.org/about-aps/finances/; Cherry Creek School District, Comprehensive Annual Financial Reports, 2006-2011, Budget 2012, https://www.cherrycreekschools.org/FiscalServices/Financial-Transparency/Pages/default.aspx; Adams 12 School District, Comprehensive Annual Financial Reports, 2005-2011, Budget 2012, https://www.adams12.org/financial_accountability/financial_transparency.

14 “Colorado Public Employees’ Retirement Association Hybrid Defined Benefit Plan,” prepared by Gabriel, Roeder, Smith & Company for the Colorado Office of the State Auditor, June 25, 2015.

15 Andrew Biggs, “Not So Modest: Pension Benefits for Full-Career State Government Employees,” American Enterprise Institute, March 2014, https://www.aei.org/wp-content/uploads/2014/03/-aei-economic-perspective-march-2014_160053300510.pdf

16 “The State of Retirement: Grading America’s Public Pension Plans,” Urban Institute, Public Pension Project, https://apps.urban.org/features/SLEPP/index.html, accessed February 3, 2016.

17 “Doing the Math on Teacher Pensions,” National Council on Teacher Quality, January 2015, https://www.nctq.org/dmsView/Doing_the_Math

18 Hybrid Plan Study, p. 37, supra note 14.

19 Hybrid Plan Study, p. 58, supra note 14.

<sup”>20 Hybrid Plan Study, p. 60, supra note 14.

21 Hybrid Plan Study, p. 61, supra note 14.

22 Alicia H. Munnell, Jean-Pierre Aubry, and Caroline V. Crawford, “Investment Returns: Defined Benefit vs. Defined Contribution Plans,” Center for Retirement Research, Boston College, December 2015, Number 15-21. https://crr.bc.edu/wp-content/uploads/2015/12/IB_15-211.pdf

23 “Sensitivity Analysis of Colorado Public Employees’ Retirement Association Hybrid Defined Benefit Plan Actuarial Assumptions,” October 2015, Pension Trustee Advisors, prepared for the Colorado State Auditor’s Office.

24 Sensitivity Analysis, p. 30, supra note 12.

25 PERA itself conducts annual sensitivity studies of the current funded level and UAAL, based on long-term returns. However, those are limited in utility, showing only the results of a narrow range of returns on a single measure of plan health.

26 Abdullah Z. Sheikh and Hongtao Qiao, “Non-normality of Market Returns: A framework for asset allocation decision-making,” for J.P. Morgan, 2009; Nassim Nicholas Taleb, The Black Swan, Chapter 15, “The Bell Curve, That Great Intellectual Fraud,” p. 229-252, Random House, New York, 2007.

27 Roger Lowenstein, “The Next Crisis: Public Pension Funds,” New York Times Magazine, June 25, 2010.

28 Andrew Biggs, “Public Pension Deficits Are Worse Thank You Think,” Wall Street Journal, March 22, 2010.

29 Biggs, “An Options Pricing Method for Calculating the Market Price of Public Sector Pension Liabilities.”

30 Michael Corkery, “Illinois Pension Fund May Cut Return Target,” Wall Street Journal, June 27, 2012.

31 John Seiler, “CalPERS Funding Might Be Only 40%,” CalWatchdog.com, March 22, 2012. https://www.calwatchdog.com/2012/03/22/calpers-funding-might-be-only-40-percent/

32 Randy Diamond, “CalSTRS’ unfunded liability rises 13%; funding ratio falls to 69.4%,” Pensions & Investing, April 9, 2012. https://www.pionline.com/article/20120409/ONLINE/120409899/calstrs-unfunded-liability-rises-13-funding-ratio-falls-to-694

33 Pennsylvania State Auditor, “Report on Municipal Pension Funds,” January 14, 2015 https://www.paauditor.gov/Media/Default/Reports/Updated%20Municipal%20pension%20special%20report_01142015_FINAL.pdf

34 Center on Regional Politics, 2012, “The Problem of Funding Pensions” Issue Memo 1, Center on Regional Politics, Temple University, Philadelphia https://www.cla.temple.edu/ipa/files/2012/12/Issue-Memo-Public-Pensions-Web-Version-092412-2-.pdf

35 Joey Ferguson, “Unions, pensions drove Stockton, California to bankruptcy,” Deseret News, June 29, 2012.

36 Wayne H. Winegarden, “Going Broke One City at a Time: Municipal Bankruptcies in America,” Pacific Research Institute, January 2014. https://www.pacificresearch.org/fileadmin/documents/Studies/PDFs/2013-2015/MunicipalBankruptcy2014_F.pdf

37 Hazel Bradford, “Strapped state pension funds take scalpel to COLAs for relief,” Pensions & Investing, June 11, 2012. https://www.pionline.com/article/20120611/PRINT/306119977/strapped-state-pension-funds-take-scalpel-to-colas-for-relief

38 Erika Niedowski, “Providence pension deal OK is headed to judge,” AP, San Francisco Chronicle, June 25, 2012.

39 Associated Press, “2 California cities approve pension cuts,” June 6, 2012.

40 Public Employees’ Pension Reform Act, AB 340 (2012). https://leginfo.legislature.ca.gov/faces/billNavClient.xhtml?bill_id=201120120AB340

41 Nava, V and Christensen, L. (Mar 13, 2015) Analysis of the California Public Employees’ Pension Reform Act of 2013 (PEPRA). https://reason.org/news/show/ca-pepra-pension-reform

42 Nevada, SB406 (2015). https://legiscan.com/NV/bill/SB406/2015

43 Nevada, AB190 (2015). https://legiscan.com/NV/bill/AB190/2015 ; S. Whaley, “Nevada PERS pension reform put off until next session,” Las Vegas Review-Journal, May 30, 2015, https://www.reviewjournal.com/news/nevada-legislature/nevada-pers-pension-reform-put-until-next-session

44 74 OK Stat § 74-935.1 (2014). https://legiscan.com/OK/bill/HB2630/2014

45 Matthew Glans, “Research & Commentary: Oklahoma Pension Reform,” Heartland Institute, August 18, 2014, https://www.heartland.org/policy-documents/research-commentary-oklahoma-pension-reform

46 Jim Malewitz, “House Plan Would Plug Hole in Pension Fund,” The Texas Tribune, March 10, 2015, https://www.texastribune.org/2015/03/10/house-leaders-pitch-plan-shore-pensions/

47 Pa. pension reform bill dies as legislative session nears end,” York Dispatch, October 27, 2016, https://www.yorkdispatch.com/story/news/local/pennsylvania/2016/10/26/pa-lawmakers-try-anew-overhaul-public-pensions/92765518/

48 James Comtois, “Pennsylvania Senate approves bill for hybrid retirement plan for new employees,” Pensions & Investments Online, December 8, 2015. https://www.pionline.com/article/20151208/ONLINE/151209883/pennsylvania-senate-approves-bill-for-hybrid-retirement-plan-for-new-employees

49 Ronald Snell, “Highlights of State Pension Reform in 2012,” for National Council of State Legislatures, July 17, 2012. https://www.ncsl.org/research/fiscal-policy/highlights-pension-reform-2012.aspx

50 Sub House Bill 2333 (2012). https://www.kslegislature.org/li_2012/b2011_12/measures/hb2333/

51 Arndy Marso, “KPERS Reform Heading to Governor,” The Topeka Capital-Journal, May 17, 2012. https://cjonline.com/news/2012-05-17/kpers-reform-heading-governor

52 Mark Desetti, “Changes Coming to Rules for Working After Retirement,” Under The Dome, May 18, 2015. https://underthedomeks.org/changes-coming-to-rules-for-working-after-retirement/

53https://www.courts.state.co.us/userfiles/file/Court_Probation/Supreme_Court/Opinions/2012/12SC906.pdf

54 Barbara A. Butrica, Howard M Iams, Karen E. Smith, and Eric K. Toder, “The Disappearing Defined Benefit Pension and Its Potential Impact on the Retirement Incomes of Baby Boomers,” U.S. Social Security Administration, Social Security Bulletin 69, No. 3 (2009). https://www.ssa.gov/policy/docs/ssb/v69n3/v69n3p1.html

55 McGee and Welch, p. 23, supra note 11.

56 Josh B. McGee, “The Transition Cost Mirage – False Arguments Distract from Real Pension Reform Debates,” Laura and John Arnold Foundation, March 2013, https://www.arnoldfoundation.org/wp-content/uploads/2014/02/LJAF_Transition_Cost_Policy_Brief.pdf

57 Barry Poulson, “Solving the Funding Crises in PERA,” Independence Institute Issue Paper 5-2012, May 2012, https://tax.i2i.org/2012/05/18/solving-the-funding-crises-in-pera/

58 Steven Malanga, “Scary Pension Math,” City Journal, Manhattan Institute, Winter 2016, https://www.city-journal.org/2016/26_1_pensions.html, retrieved February 10, 2016:

“Because its goals were modest, [in 1932] California required [CalPERS] to limit its investments to secure government securities with a guaranteed return.…In 1970, it lowered the retirement age to 60. To help pay for the largesse, the state, beginning in the 1960s, let CalPERS start speculating in real estate and stocks—riskier bets but with potentially higher returns than government securities. Over time, California raised the amount of assets that the pension fund could put into such investments.”

59 Ed Mendel, “CalSTRS, CalPERS okay risk reduction,” Capitol Weekly, November 23, 2015, https://capitolweekly.net/calpers-calstrs-risk-reduction-plans/

60 McGee and Welch, p. 14, supra note 11.

61https://tax.i2i.org/citizens-budget/

62 PERA Shareholder Meeting, November 22, 2010. https://www.youtube.com/watch?v=lCpW8R39Mt0&t=840s.

63 TRACER Search, June 17, 2013; The Colorado Secretary of State requires lobbyists to register on TRACER, and to record any time they are instructed by a client to take a position favoring, opposing, or monitoring a bill.

64 Nicholas Confessore, “Donations to Key Cuomo Ally Show a Rift Among Unions,” New York Times, June 7, 2012; Angela Delli Santi and Beth DeFalco, “NJ gov, Senate leader, reach union benefits deal,” AP, June 8, 2011.

65 Walter Russell Mead, “Time to Occupy State Pensions?” Via Meadia Blog, The American Interest, June 25, 2012.

Copyright ©2016, Independence Institute

INDEPENDENCE INSTITUTE is a non-profit, non-partisan Colorado think tank. It is governed by a statewide board of trustees and holds a 501(c)(3) tax exemption from the IRS. Its public policy research focuses on economic growth, education reform, local government effectiveness, and constitutional rights.

JON CALDARA is President of the Independence Institute.

DAVID KOPEL is Research Director of the Independence Institute.

JOSHUA SHARF is a policy analyst for the Independence Institute’s Fiscal Policy Center. A web developer in private practice, his professional background includes intelligence and defense analysis, and he holds an MBA and a MS in Finance from the University of Denver. He was twice a candidate for the Colorado House of Representatives from the Denver area.

ADDITIONAL RESOURCES on this subject can be found at: https://www.i2i.org/fiscal

NOTHING WRITTEN here is to be construed as necessarily representing the views of the Independence Institute or as an attempt to influence any election or legislative action.

PERMISSION TO REPRINT this paper in whole or in part is hereby granted provided full credit is given to the Independence Institute.

[/vc_column_text][/vc_column][/vc_row]